The region is at a crucial point in its economic development, stuck in the so-called "middle-income trap", a state of stagnation where, despite economic growth, countries are unable to make the leap to a high-income economy due to structural barriers.

What is the middle-income trap?

The middle-income trap occurs when a country achieves initial economic growth but is soon slowed by several factors, such as competition from countries with lower production costs and a lack of innovation and productivity improvements. The region has experienced this phenomenon, as it has not been able to consolidate sustained growth that would propel it to high economic income.

Looking at the performance of per capita Gross Domestic Product (GDP) growth adjusted for purchasing power parity during the last decade, the Central American region reflected a diversity of performances, where Panama stood out maintaining an annual per capita GDP growth rate of 3.75%, the highest among its neighbors and following a trend of sustained growth since the 1990s. Costa Rica, although with a slight slowdown, continued to show a stable economy with an average annual increase of 2.50%.

Meanwhile, Nicaragua and Honduras managed to reverse the lower trends of the 1990s, improving their figures to growth rates of 2.14% and 1.57% per year respectively in the 2010s, showing significant economic progress. El Salvador and Guatemala, which make up the intermediate group, also experienced improvements compared to the previous decade, registering growth rates of 2.05% and 1.82% per year, respectively.

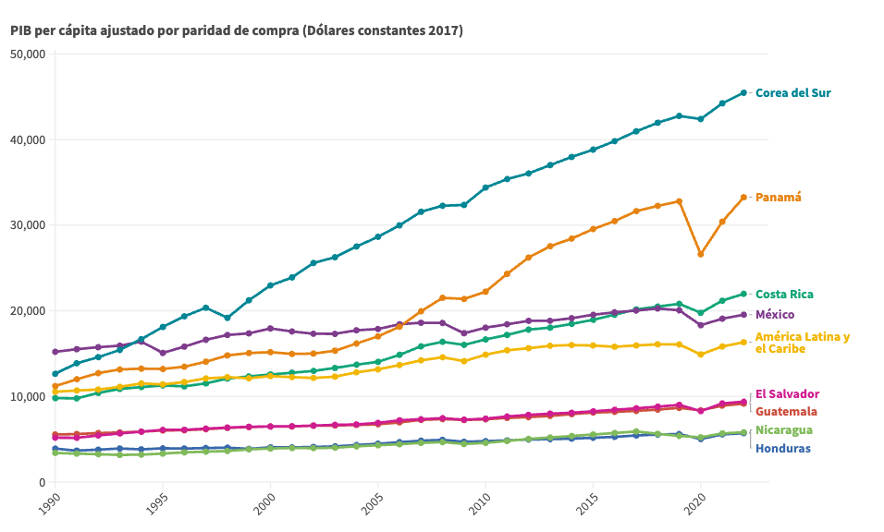

Has this performance been good? Comparing with South Korea, a country that came out of the middle-income trap, we find that in 1990 it had a GDP per capita adjusted by purchasing parity of 12,656 dollars (constant 2017), barely higher than Panama's 11,212 dollars and Costa Rica's 9,811, but the Asian country had in that decade 6.02% average growth. Thus, 30 years later, in 2022 South Korea has a GDP per capita of 45,467 dollars, with a high level of income, and with a figure much higher than the 33,266 dollars of Panama and 21,987 dollars of Costa Rica, the two countries with the highest per capita income in the region (see Figure 1).

Figure 1. Source: Own calculations with data from the World Bank.

How to get out of the trap?

The data show that we are growing, but we are still dealing with fundamental challenges that restrict sustained and significant growth to make the leap, since the growth we have had is a result of insufficient investment in innovation and technology, education and human capital formation that does not meet global expectations, inadequate infrastructure, economic and social inequalities, and a deficient business and governance environment. In this regard, the following changes are required:

Innovation for competitiveness: Supporting research and development and promoting collaboration between the private sector and academic institutions to stimulate global competitiveness. Recalling that the capacity to innovate determines the long-term competitiveness of an economy in the global marketplace.

Future-oriented education: Invest in quality education and technical training aligned with international labor market needs and technological trends. Although there have been improvements in enrollment rates, the quality of education and the development of advanced skills still lag behind high-income economies.

Improved infrastructure: Prioritize infrastructure development to increase efficiency and attract investment. Ensuring proper functioning and resilience to natural disasters.

Social inclusion: Implement policies that address inequality and promote an equitable distribution of income and opportunities. Urban-rural inequalities and inequalities between different social groups perpetuate poverty and limit domestic demand, which is critical to sustain growth.

Better institutions: Simplify bureaucratic processes and strengthen law and order to improve the business environment and attract investment; i.e. ensure certainty. Excessive bureaucracy, corruption and political instability deter foreign direct investment and weaken confidence in the local business environment.

Having clear goals

Of course, escaping the middle-income trap is not a simple task; it is social, technological, economic and institutional issues that need to be addressed. This means having a sustained commitment to clear and coherent policies that address the roots of economic inertia. And doing so in an uncertain, vulnerable, risky and ambiguous global context further complicates the scenario. But at the same time, it is clear that inaction or complacent incremental progress are not viable options; a dynamic and comprehensive strategy is required to address these challenges with the urgency and seriousness they deserve. Achieving a region with greater income and social progress in the coming years will depend on our truly understanding that change and acceleration are urgently needed to prosper.